Joe Hockey famously advised first home buyers to “get a good job that pays good money”. How about the top job? The Prime Minister of the Commonwealth of Australia earns no less than $507,000 a year. That’s got to give us some serious buying power, right? How much could you really afford in the PM’s home town of Sydney?

First things first, we need to pay tax. Assuming we haven’t got a handful of negatively geared properties already, our tax bill is $202,000. That leaves us $301,000 though, which is still more money than most first home buyers can dream of.

To avoid mortgage stress, your mortgage repayments should be less than 30% of your income, or about $92000. Of course we’ll be getting our loan at the great Microburbs rate of 3.89%.

According to the government’s own MoneySmart calculator, annual repayments of $92,000, at 3.89% gives you borrowing power of… $1,450,000.

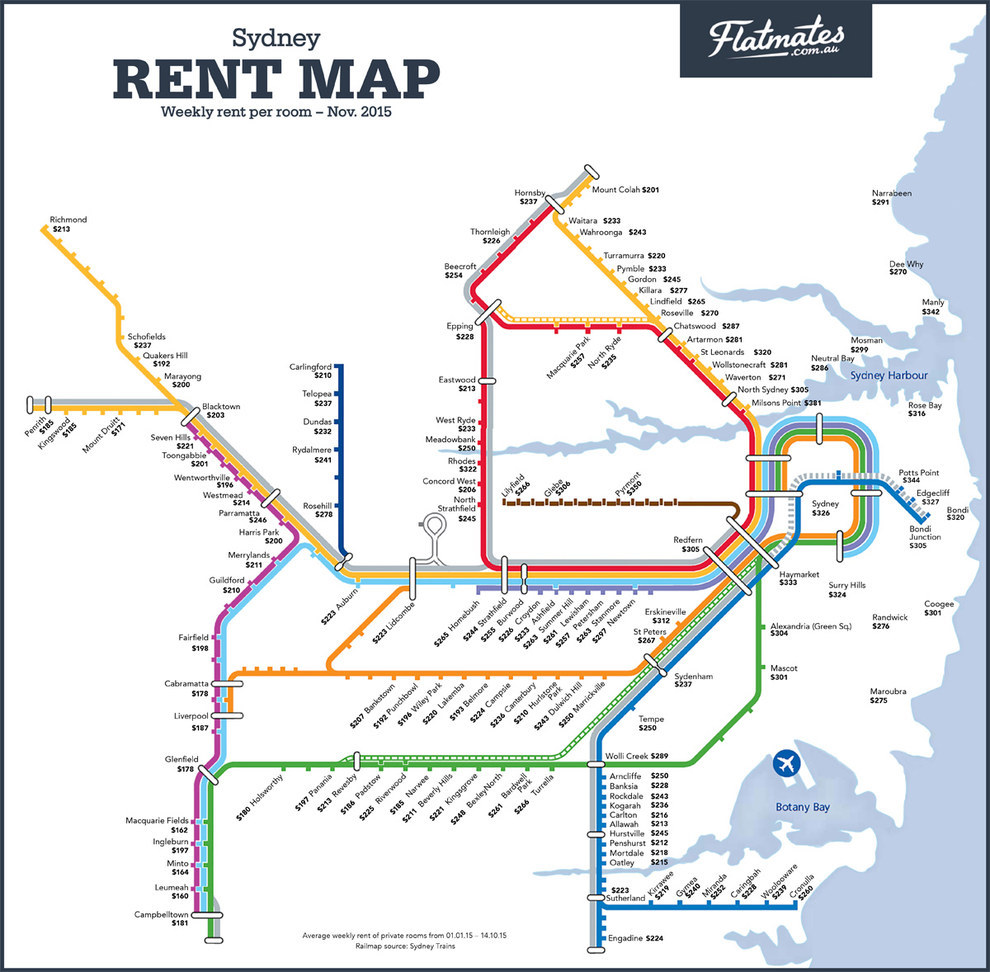

Wait a minute. That’s not very much really. The median house price in Sydney is around $1,000,000. The median prices in 172 Sydney suburbs is over our budget!

Naturally anything in Sydney with a view of the Harbour, close to beaches or close to the CBD is off the table. Likewise, the inner west, north shore and more affluent parts of suburbia are way out of your reach.

North western suburbs like Cheltenham, Beecroft and Pennant Hills may be out, but if you’re prepared to go a little further, Castle Hill is a mere 26 km to the city and is still in your budget until the metro opens there in 2019.

Houses in Strathfield are out, but neighbouring Burwood would be ok. Dulwich Hill has become too popular for the likes of the PM, but Hurlstone Park or Ashbury, beyond the reach of the light rail, are still options.

That’s not to say there aren’t some houses below the median price in inner areas.

This inner west terrace house is almost within our budget, with an auction guide price of $1,500,000. Could this fixer-upper be our answer to the Whitehouse or Number 10?

Over to the Microburbs Property Report to find out!

This inner west terrace has a hip score of 8 and an affluence score of 10. Unfortunately it only scores a 4 for safety, so we may need to put on a few more protective services officers.

Of course there’s still the deposit. You’ll need about 3 years of PM’s pay to get that together. Unfortunately, nobody has been able to last in that job that long in nearly a decade.

If you find your mortgage a pain too, you can at least get a better interest rate. Get access to our exclusive lenders and reduce your rate to as low as 3.89% now!